Accurate revenue recognition is the cornerstone of financial reporting for any business. It ensures that the income generated from sales of goods or services is recorded in the correct accounting period, reflecting the true financial health of the company. This is particularly crucial when dealing with customer deposits and deferred revenue, as premature or delayed recognition can distort financial statements and mislead stakeholders. Reconciling customer deposits is a critical accounting process that ensures the accuracy of a company’s financial statements. When customers make deposits, these amounts are not yet revenue but rather liabilities that the company owes until the service is performed or the product is delivered. The reconciliation process involves verifying that the recorded deposits match the actual cash received and are accounted for correctly in the general ledger.

Bank’s Debits and Credits

This process is essential for maintaining the integrity of financial records and can be complex, especially for businesses with a high volume of transactions. Deferred revenue, also known as unearned revenue, represents a prepayment by customers for goods or services that are to be delivered or performed in the future. The recognition of deferred revenue has a significant impact on a company’s financial statements, affecting the balance sheet, income statement, and cash flow statement. The best advice is to invest in accounting software like Xero; in the end, you will enjoy the accounting process, save time, and generate accurate financial records.

Step 3: Create a trust liability bank account (Not always needed)

In Connected, a „Miscellaneous“ type Receipt is used to record a customer deposit. This could be used either as lump sum payment against any outstanding existing transactions or as a deposit against a future transaction. Customer deposits can significantly influence a company’s cash flow, providing an influx of cash before the actual sale occurs. This immediate liquidity can be advantageous for managing day-to-day operations, purchasing inventory, or investing in capital improvements. However, it’s important to remember that these funds are not a reflection of earned revenue and should not be used indiscriminately.

Understanding the Accounting Principles Behind Deferred Revenue

The transaction reverses the customer deposit from the balance sheet. But instead of paying cashback to the customer, it is used to net off with the accounts receivable. The company record accounts receivable of only $ 70,000 due to the deduction of $ 30,000 from the total purchase price. The journal entry is debiting cash received and credit customers’ deposits.

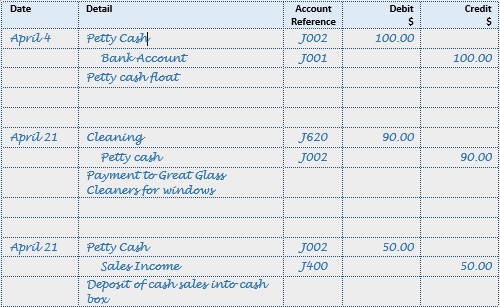

Receiving a Prepayment Deposit

Liabilities also include amounts received in advance for a future sale or for a future service to be performed. As a result these items are not reported among the assets appearing on the balance sheet. If you are new to the study of debits and credits in accounting, this may seem puzzling. After all, you learned that debiting accounts payable solutions the Cash account in the general ledger increases its balance, yet your bank says it is crediting your checking account to increase its balance. Similarly, you learned that crediting the Cash account in the general ledger reduces its balance, yet your bank says it is debiting your checking account to reduce its balance.

QuickBooks Does Not Print Bill Payments

It will be net off with the accounts receivable that company has to collect from the customers. A liability account on the books of a company receiving cash in advance of delivering goods or services to the customer. The entry on the books of the company at the time the money is received in advance is a debit to Cash and a credit to Customer Deposits.

Some businesses receive retainers or deposits from customers before performing any services. When they invoice customers for services, those invoices are paid using the money from the deposits. As apparent in the above journal entries, the accounting for cash deposits is straightforward. As long as the company can identify the source of the deposited sum, it can use it as a credit entry. Anytime there is a customer deposit account, remember that it will be treated as a current liability. It happens when the goods and services provided are within a year; it becomes a long-term liability when it is a more extended period.

She pays a $1000 deposit in advance to ensure the dress is held for her while alterations are made. This prepayment is held by the company, with any remaining fee paid at the time that the dress is completed and handed over. If the company is unable to provide the promised goods or services, the deposit must be refunded. You’ve paid money toward a rug that you do not yet have, so technically, it’s not an expense yet. But your cash account has decreased, and this has to be reflected in your records.

However, the underlying bank account to which a company adds this balance may vary. When you receive cash from a customer before providing goods or services, how is this accounted for? Here’s a closer look at how to account for deposits from customers, including the correct category to record them under. If you are the business that ordered the rug for your office, you also must record the journal entry for the deposit, because this was a business expense. You agreed to pay $750 as a deposit on the rug, and you agreed to pay the balance when the rug was completed.

- Receiving and accounting for advance payments from a client is a task that requires careful attention to the way entries are made in a company’s accounting records.

- When the company provides goods or services to the customers, they need to record revenue as well.

- Recognizing customer deposits in the accounting world is a critical step that ensures revenue is recorded accurately.

Since the bank has not earned this money, the amount is recorded by the bank with a debit to its asset account Cash and a credit to the bank’s liability account Customer Deposits. The company receiving a customer deposit initially records the deposit as a liability. Once the company performs under its contract with the customer, it debits the liability account to eliminate the liability, and credits a revenue account to record the sale. This may occur in stages, if deliverables are sent out over a period of time.

Schreibe einen Kommentar